Bybit XAUT Options: 4 strategies for defined-risk gold exposure

Gold remains a core macro asset, but spot exposure, ETFs and perpetual contracts do not offer the same payoff flexibility as options. XAUT Options allow traders to structure directional or volatility views on gold, with defined maximum loss for buyers and more complex, actively managed risk for sellers. XAUT Options are European-style and cash-settled in USDT — meaning they can only be exercised at expiry, and settlement is in cash rather than physical delivery of gold tokens.

This article walks through four practical strategy frameworks for XAUT Options: directional calls and puts, vertical spreads, premium selling and event-driven straddles/strangles. For each, we cover when to use it, how to size it relative to gold's macro calendar and how to evaluate implied volatility conditions before entering.

Key Takeaways:

XAUT Options allow traders to structure gold exposure with defined maximum loss (buyers) or actively managed, quantifiable risk parameters (sellers).

Gold's event-driven nature can create differences between implied and realized volatility, which options traders may consider when selecting strategies.

Strategy selection depends on your market view: directional conviction → single-leg or spread; no strong directional view + elevated IV + clear risk controls → premium-selling strategies; binary event approaching → straddle/strangle.

Risk Disclaimer: This article is for informational purposes only and does not constitute financial advice. All numerical examples are illustrative only and do not represent live prices, recommended allocations, or guaranteed outcomes. Options trading involves substantial risk of loss. Sellers of options face losses that can exceed the premium received, potentially significantly. Past market behavior does not guarantee future results. |

When does gold's behavior favor options over spot?

Gold tends to move in regime shifts — extended consolidation phases punctuated by sharp macro-driven moves triggered by rate decisions, geopolitical shocks or inflation surprises. This pattern has important implications for how you structure exposure.

During consolidation periods, holding spot or perpetual positions can mean paying funding costs while P&L goes nowhere. Options offer two distinct ways to address this:

As a buyer: Define your cost of being wrong. A long call or put limits your downside to the premium paid while you wait for your thesis to play out.

As a seller: Structure premium-selling strategies when implied volatility appears elevated relative to expected realized volatility, though this requires active management and carries the risk of losses exceeding premium received.

Gold's implied volatility, tracked via the CBOE Gold Volatility Index (GVZ), tends to spike around identifiable macro events: FOMC meetings, CPI releases and geopolitical escalation. These events appear on a structured calendar in advance, even if direction and magnitude remain uncertain. This makes XAUT Options more amenable to calendar-aware strategy selection compared to assets driven by unpredictable catalysts.

Key concept: The GVZ (CBOE Gold Volatility Index) represents the market's implied expectation of future gold volatility, derived from GLD options. When GVZ is high relative to what you expect gold to actually move (realized volatility), options appear expensive. When GVZ is low relative to your expected move, options may appear cheap — but "cheap" and "expensive" are assessments, not certainties.

Strategy 1 — Directional calls and puts (Defined-risk conviction trades)

When to use

Directional single-leg options are appropriate when you have a specific thesis about gold's direction tied to an identifiable catalyst — for example, anticipated rate cuts (bullish), geopolitical escalation (historically bullish) or a strong dollar environment (historically bearish). The advantage over spot: your maximum loss is precisely defined before you enter.

How it works

Buying a Call: Profits if XAUT rises above the strike by more than the premium paid. Maximum loss is the premium plus fees. Potential upside is theoretically uncapped above the breakeven.

Buying a Put: Profits if XAUT falls below the strike by more than the premium paid. Maximum loss is the premium plus fees. Maximum gain is limited by how far the underlying can fall (toward zero).

Strike selection framework

Strike type | Characteristics | Best suited for |

At-the-money (ATM) | Higher probability of finishing in-the-money; higher premium cost | High-conviction views where cost is secondary |

3–5% OTM | Lower upfront cost; requires a moderate directional move | Moderate conviction; balanced cost vs. probability |

8–10% OTM | Cheapest premium; lowest probability; highest risk of expiring worthless | Tail-risk hedges or speculative views on large moves |

Expiry selection

Align your expiry with your catalyst window. If your thesis depends on the next FOMC decision, select an expiry 1–3 days after the event to allow the move to develop. Gold catalysts are often scheduled events, which makes expiry alignment more tractable than in crypto-native markets where catalysts can be sudden. Longer expiries give your thesis more time to play out but cost more in premium.

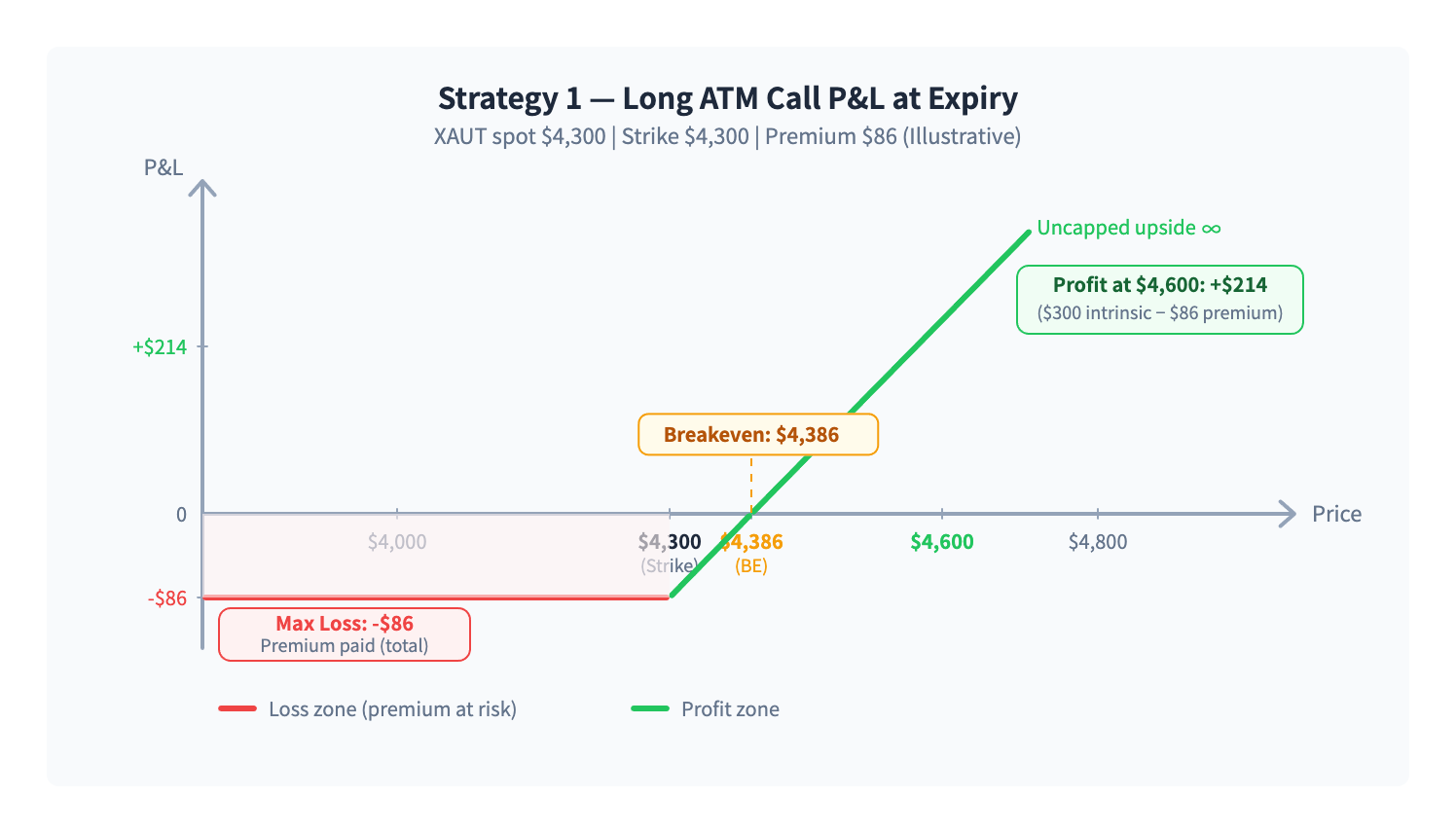

Illustrative example (Bullish scenario)

Illustrative only — not live prices or recommendations

XAUT spot: $4,300 | Buy 1 ATM Call, strike $4,300, premium $86, expiry in 14 days

Maximum loss: $86 (premium paid) — occurs if XAUT closes at or below $4,300 at expiry

Breakeven: $4,386 at expiry

Profit at $4,600: $300 − $86 = $214 per option

Maximum gain: Theoretically uncapped above breakeven

XAUT options strategy 1 — Long ATM Call P&L at expiration

Strategy 2 — Vertical spreads (Capped cost, capped reward)

When to use

Vertical spreads are appropriate when you have a directional view but want to reduce your upfront premium cost compared to a naked long option. The trade-off: your maximum gain is also capped. Spreads can be useful when you believe gold will move directionally but not dramatically beyond a certain range.

How it works

Bull call spread: Buy a lower-strike Call, sell a higher-strike Call. The premium received from the short leg reduces your net cost. You profit if XAUT rises above the lower strike, with maximum gain at or above the higher strike.

Bear put spread: Buy a higher-strike Put, sell a lower-strike Put. Same logic for a bearish view — reduced cost, capped downside profit.

P&L structure

Scenario | Bull call spread outcome |

Both legs expire OTM | Maximum loss = net premium paid |

XAUT between strikes at expiry | Partial profit; long leg has value, short leg expires worthless |

XAUT at or above upper strike | Maximum gain = spread width minus net premium paid |

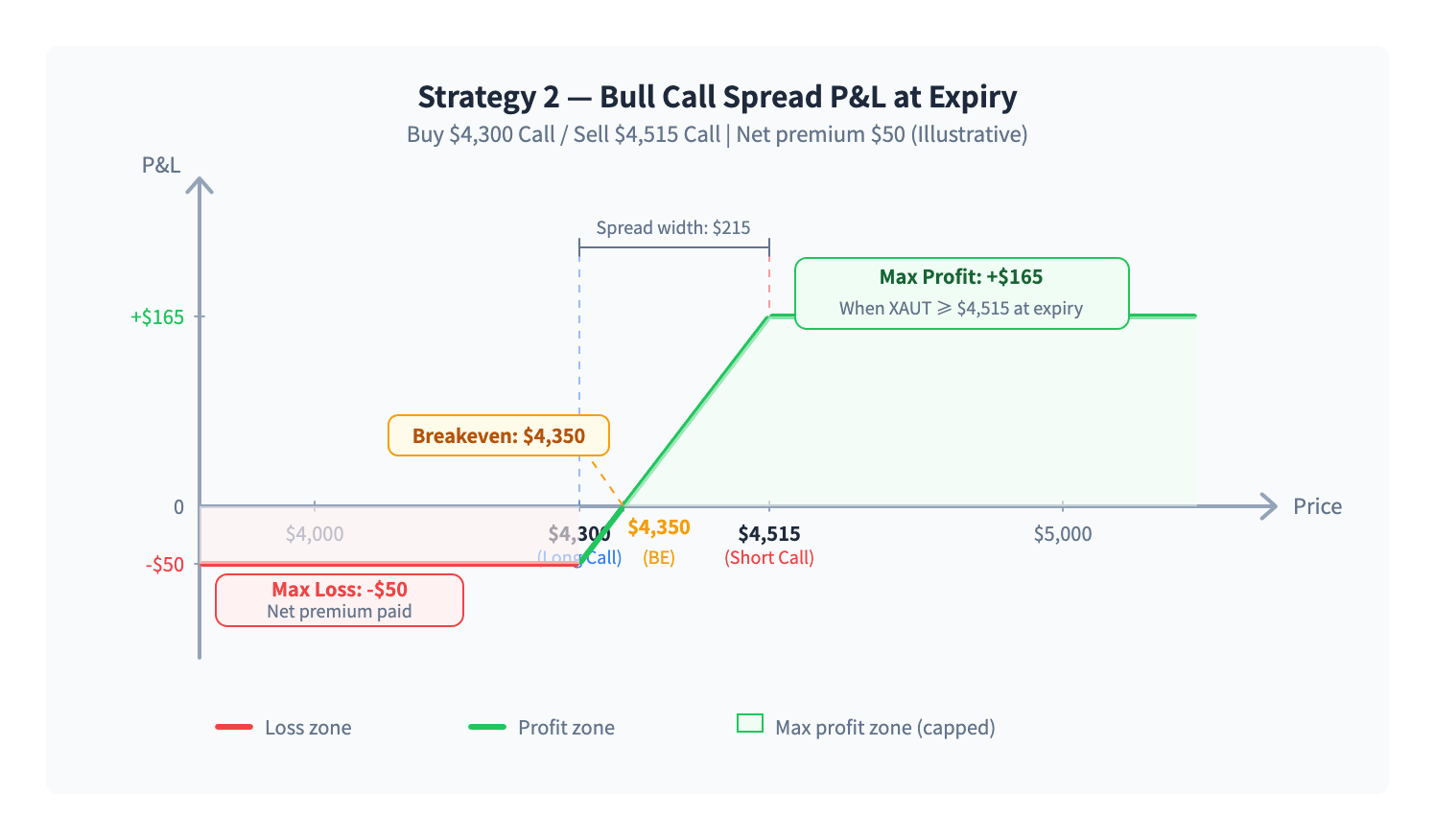

Illustrative example (Bull call spread)

Illustrative only — not live prices or recommendations

XAUT spot: $4,300 | Buy $4,300 Call at $86, Sell $4,515 Call at $36 | Net premium: $50

Maximum loss: $50 (net premium paid) — occurs if XAUT closes at or below $4,300

Breakeven: $4,350 at expiry

Maximum gain: $215 − $50 = $165 — occurs if XAUT closes at or above $4,515

When max profit reached: At expiry with XAUT ≥ $4,515

XAUT options strategy 2 — Bull call spread P&L at expiry

Spread width calibration

Historical gold moves around similar macro events can inform spread width selection. For example, if gold has historically moved ±2–4% around FOMC decisions, positioning the upper strike near the high end of that historical range may align with moderate conviction. However, historical data is informational only. Past move magnitudes do not predict future ones, and any single event can produce a move well outside the historical range in either direction.

Strategy 3 — Premium selling (Assessing volatility mismatch)

Critical risk warning: Selling options carries the potential for losses that significantly exceed the premium received. This is not a passive or low-risk strategy. It requires active monitoring, pre-defined exit triggers and disciplined position sizing. If you cannot monitor the position actively, do not sell options.

Core logic

When implied volatility appears elevated relative to what you expect gold to actually realize, selling options allows you to collect premium. The strategy profits if XAUT stays within the range defined by your short strikes through expiry. However, if gold moves sharply, particularly on an unexpected macro event, losses can significantly exceed the premium collected.

Common structures

Selling OTM Puts: Collect premium; profit if XAUT stays above your short strike. Loss if XAUT drops sharply through the strike.

Selling OTM Calls: Collect premium; profit if XAUT stays below your short strike. Loss if XAUT rallies sharply through the strike.

Short strangle: Sell both an OTM Put and an OTM Call. Collect premium from both legs; profit if XAUT stays within the range. Loss if XAUT moves sharply in either direction.

XAUT-specific context

The GVZ tends to spike around macro events and then mean-revert once the event resolves without further escalation. The period after a volatility spike resolves may present an environment where implied volatility is relatively elevated compared to the quiet that follows, but this is a probabilistic observation, not a reliable edge. Every premium-selling decision requires its own risk assessment.

Position sizing

Define a maximum risk budget per trade before entering. Avoid concentrating a large share of account NAV in short-volatility exposure, as multiple simultaneous short positions can behave similarly in a macro shock. The examples below are illustrative only (these are not recommended allocation sizes).

Illustrative sizing framework (not a recommendation):

Example (Short Strangle): XAUT spot $4,300 | Sell $4,085 Put at $65 + Sell $4,515 Call at $65 | Total premium: $130

• Max profit: +$130 (XAUT closes between $3,955–$4,645 at expiry)

• Lower breakeven: $3,955 | Upper breakeven: $4,645

• If XAUT falls to $3,700 at expiry: short put loss = $385, minus $130 premium = net loss −$255

• If XAUT rises to $4,900 at expiry: short call loss = $385, minus $130 premium = net loss −$255

Sizing: with account size $10,000 and a max loss budget of $300 (3% of NAV, illustrative only), model the price breach level where your net loss hits −$300 (roughly $3,685 on the downside or $4,915 on the upside in this example) and set that as your exit trigger — not expiry.

XAUT options strategy 3 — Short strangle P&L at expiry

Short-dated positions and gamma risk

Rolling short-dated positions (1–3 day expiry) limits exposure to calendar decay, but introduces significant gamma risk. Gamma measures how rapidly delta changes as the underlying moves. For short-dated options near the strike, a sharp intraday move in XAUT can cause delta to shift rapidly, potentially generating losses faster than you can react. Short-dated premium selling is not inherently lower risk than longer-dated — it trades one risk dimension for another.

Exit discipline (Non-negotiable)

Pre-define your exit triggers before entering any short position. Do not rely on judgment in the moment. Specific triggers to define in advance:

XAUT price reaches a specific breach level relative to your short strike

GVZ spikes beyond a threshold that changes your volatility mismatch assessment

An unexpected geopolitical escalation or macro data release occurs

Your loss on the position reaches a pre-defined maximum

Never add to a losing seller position without fully re-evaluating the thesis. Adding to a short position that is moving against you increases risk at exactly the wrong time. This is one of the most common errors in options selling.

Strategy 4 — event-driven straddles and strangles (Playing volatility expansion)

When to Use

When a major macro event is approaching but the direction of the move is genuinely uncertain, buying a straddle or strangle allows you to profit from a large move in either direction — provided the move exceeds the combined premium paid for both legs.

Straddle: Buy an ATM Call + ATM Put with the same strike and expiry. Higher premium, profits from any large move.

Strangle: Buy an OTM Call + OTM Put. Lower combined premium, but requires a larger move to profit.

Gold's macro event calendar

Gold's primary catalysts (FOMC decisions, CPI releases, geopolitical escalations) appear on a structured calendar. This makes straddle/strangle timing more systematic than in pure crypto markets. However, the direction and magnitude of gold's response to any specific event remains uncertain. A "large" event by any historical measure can still produce a small or muted gold move.

IV crush: The primary risk

IV crush is the most common way event trades lose money — even when you are right on direction.

Before major events, implied volatility typically rises as market participants buy options for protection or speculation. After the event resolves, implied volatility often collapses sharply, even if gold moves in the direction you expected. If the IV decline exceeds the intrinsic value gained from the directional move, your options can lose value despite being "right."

Example: You buy a straddle before FOMC. Gold moves 1.5%, but the straddle costs 2.5% of spot in premium. Even with the move, you lose. Additionally, IV drops 30% after the announcement, further reducing option values beyond just time value.

Timing considerations

Entry timing relative to the event matters significantly. Implied volatility often begins rising days before a major event, increasing straddle/strangle costs progressively. Entering too early means paying less premium but waiting longer through time decay. Entering too close to the event means paying elevated IV that is more likely to crush after. There is no universally correct timing. It depends on your assessment of where IV is relative to expected move magnitude.

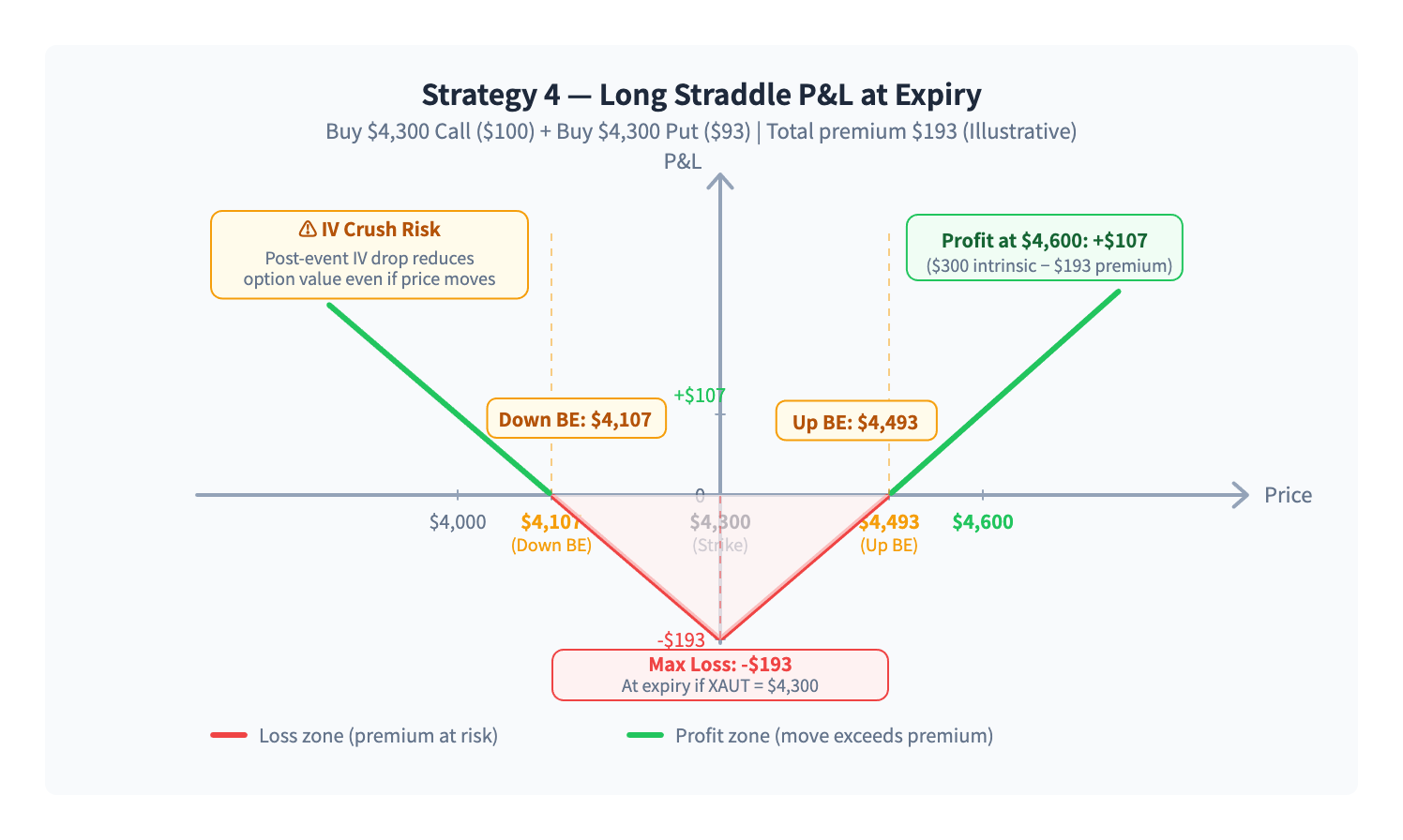

Illustrative example (Straddle on FOMC)

Illustrative only — not live prices or recommendations

XAUT spot: $4,300 | Buy $4,300 Call at $100, Buy $4,300 Put at $93 | Total premium: $193

Maximum loss: $193 — occurs if XAUT closes exactly at $4,300 at expiry

Upside breakeven: $4,493 at expiry

Downside breakeven: $4,107 at expiry

Profit scenario: XAUT moves to $4,600 (+7.0%) at expiry — Call value $300, Put value $0, P&L = $300 − $193 = $107

IV crush scenario: XAUT moves to $4,472 (+4%) but IV drops sharply post-event. Despite being directionally correct, option values fall due to IV collapse and time decay

XAUT options strategy 4 — Long straddle P&L at expiry

Comparing cost vs. historical move magnitude

Before entering an event-driven straddle or strangle, compare the total premium paid to gold's historical move magnitude for that event type. If FOMC decisions have historically moved gold ±1–3%, and a straddle costs 4% of spot in premium, the historical data suggests the cost exceeds typical move magnitude. This does not mean you should not enter — outlier moves happen — but it frames the risk clearly. Historical data is informational, not predictive.

Risk management framework

By strategy type

Strategy | Key risk considerations |

Long options (calls/puts) | Maximum loss is defined (premium paid), but premium is still capital at full risk of total loss. Defined loss does not mean low risk. |

Spreads | Monitor assignment/exercise mechanics if relevant. European/cash-settled structure reduces operational complexity at expiry. |

Short options | Margin requirements can change as price and volatility move. Losses can significantly exceed premium received in fast markets. |

Event straddles/strangles | Account for IV crush after the event — this is the primary risk for buyers, even when directionally correct. |

Universal guidelines

Check liquidity before entering: Assess bid-ask spreads and available expiries. Wider spreads increase your effective entry cost and reduce exit flexibility. For large orders or multi-leg strategies (spreads, straddles, strangles) where executing legs individually may result in significant slippage, XAUT Options are available on Bybit RFQ, allowing you to request a single quoted price for the full structure.

Account for existing exposure: If you already hold spot XAUT or gold exposure elsewhere, your options positions should account for that correlation. You may be doubling directional risk without realizing it.

Set a "stop clock" for long positions: If your thesis hasn't developed by a defined portion of time remaining to expiry, evaluate closing the position to recover remaining time value rather than letting it decay to zero.

Pre-define exit triggers for short positions: Price breach levels, GVZ spike thresholds, news triggers. Write these down before entering.

Never add to a losing short position without re-evaluating the thesis from scratch.

The bottom line

XAUT Options let traders match their strategy to their specific market view on gold, from simple directional bets with defined risk to premium-selling frameworks and event-driven volatility plays. The key is choosing the right structure for the right environment and applying disciplined risk management regardless of strategy type.

Gold's macro-driven, event-calendar nature makes strategy selection more structured than in pure crypto markets. But uncertainty in direction and magnitude always remains. No strategy eliminates risk — each one trades one form of risk for another. Understanding that trade-off is the foundation of sound options strategy.

Next steps: Explore XAUT Options on Bybit | Trade multi-leg strategies via Bybit RFQ | Read the latest Options Weekly for market commentary and strategy context. |

#LearnWithBybit