Bybit Options Weekly Review: May 19–May 25

TL; DR

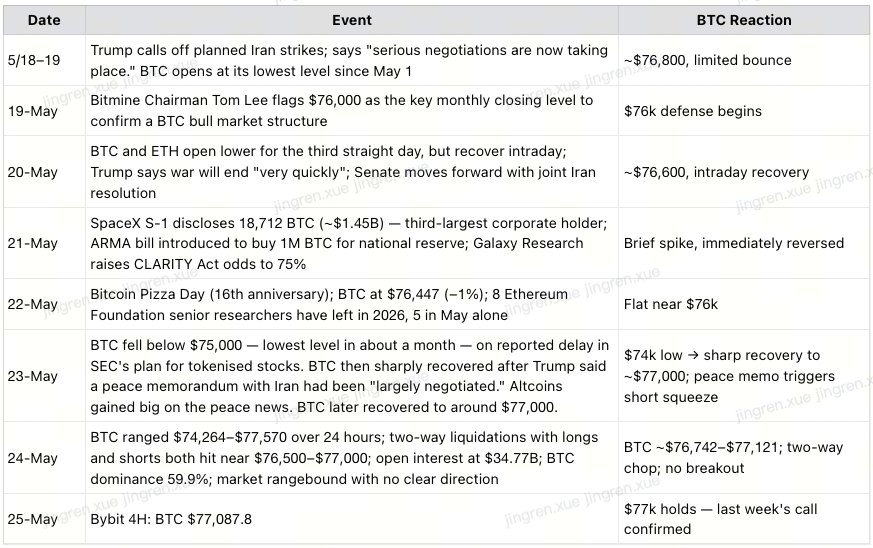

Last week's call validated in full: BTC touched the $74k dense support zone floor, and recovered and now still hovering around 77k- exactly as mapped.

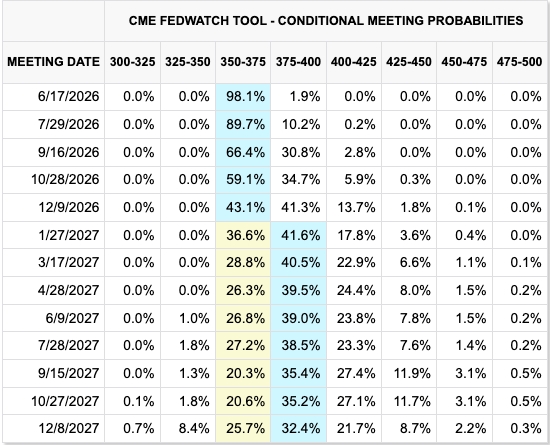

We flagged the rate hike headwind last week. This week Nomura withdrew its rate cut forecast and hike odds surged to 60%. Confirmed.

DVOL pushed further to ~35% — a new cycle low. Historically extreme. This level is rare in BTC's history.

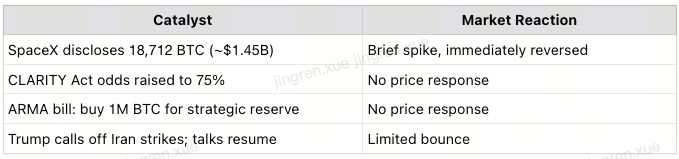

SpaceX disclosed 18,712 BTC (~$1.45B). ARMA bill proposes buying 1M BTC for a national reserve. CLARITY Act odds at 75%. Catalysts stacking — price not responding.

The most important macro finding of the week: peace does not mean lower rates. Barclays, Goldman, ING, and JPMorgan all confirm — this yield cycle is structural, driven by debt, AI investment, and a rising neutral rate. The "ceasefire → rate cuts → BTC rallies" logic chain is broken.

Fibonacci 0.382 ($74k) is holding. $78,500 is the gatekeeper. $73,500–$75,500 is the double support floor below.

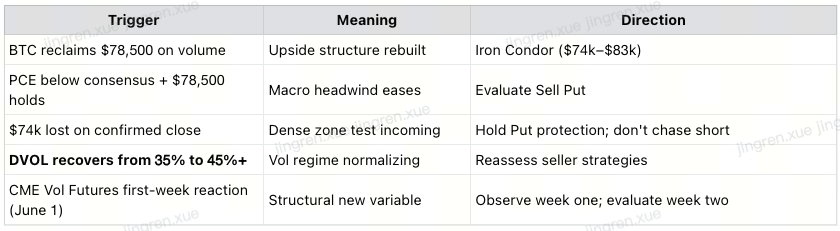

No strategy recommendation. Waiting for DVOL to recover above 45% before re-engaging.

I. Weekly Market Recap

Price Action (Bybit, updated May 25, 3:32 UTC):

BTC carved out a $74,000–$77,500 range for the week — dipping into the dense support zone before recovering and closing nearly flat. ETH and XAUT followed a similar pattern but lagged BTC on the recovery.

Event Timeline:

II. Last Week's Calls — Validated

III. Technical Picture (Bybit 4H, May 25)

BTC: Fibonacci retracement from $60k (Feb low) → $82,765.1 (May high)

Dense trading zone: $73,500–$75,500 — formed in March–April 2026, validated repeatedly. This week's $74k low recovered squarely within this zone.

The structure in plain terms:

Hold $74k (Fib 0.382) → technical structure intact; wait for direction

Reclaim $78,500→ upside structure rebuilds; path to $80k–$82.7k

IV. The Most Important Macro Finding: Peace ≠ Lower Rates

We called this last week: "The Fed has been repriced from 'when will they cut' to 'will they hike' — the most fundamental structural change in the macro landscape." This week's events confirmed it.

Barclays, Goldman Sachs, ING, and JPMorgan all issued warnings this week with the same conclusion: U.S. Treasury yield rises are not purely war-driven. Even if geopolitical risk premiums fade, long-term rates will stay elevated.

The three structural drivers Barclays identifies — none of which go away with a ceasefire:

1. Expanding government debt — Trump's tax cuts on already-elevated debt means more Treasury issuance

2. Rising neutral interest rate — AI is structurally shifting the economy's natural rate higher

3. Near-term AI investment inflation — data center buildout and semiconductor demand surge are inflationary now

ING's Padhraic Garvey: even if Hormuz reopens and inflation expectations ease, "if real yields stay elevated, long-term rates are likely to remain at high levels." The 10-year yield's break above 4.5% was "almost entirely" driven by real rates — it nearly hit 4.70% in May before pulling back.

JPMorgan CEO Jamie Dimon: rates could be "much higher than current levels." Goldman's Phillip Lee: persistent deficits and debt sustainability concerns are forcing investors to demand higher compensation on long-dated bonds.

The logic chain that is now broken:

Global Insight's Jamie Rush: "The past fifty years saw rising savings and falling investment demand push rates lower. That trend is now reversing. Rates may be structurally higher than what people became accustomed to after the financial crisis."

V. Rate Hike Odds at 60% — The Market Has Front-Run the Fed

CME's FedWatchTool is still implying a ~60% odds of rate hike in Dec 2026

Nomura's move is not noise — it is a major institution systematically repricing structural inflation and fiscal expansion. The rate hike cycle has been priced in before the Fed has spoken.

VI. Bullish Catalysts Stacking. Price Not Moving.

"Strong catalysts, no price response" = the market is absorbing overhead supply. Long-term narrative strengthening. Near-term tradability deteriorating. The pattern is consistent.

VII. Outlook for Next Week (May 26 – June 1)

PCE data + CME Volatility Futures launch (June 1) — two structural events in the same week.

Three Scenarios:

VIII. Strategy: DVOL at 35%, Still Watching

No strategy recommendation this week.

DVOL is keeping trending lower

Re-engagement triggers (watch carefully next week):

Closing Summary

① $77,000 tug-of-war fully validated. BTC touched $74,000 dense zone floor, recovered, and is holding above $77k. Technical structure intact. Direction unresolved. ② We called the rate hike headwind last week. Nomura confirmed it this week. 60%+ hike odds. The "ceasefire = rate cuts = BTC rallies" logic chain is broken. Structural high rates — driven by debt, AI, and a rising neutral rate — are not a geopolitical story. Subsiding military conflicts do not fix them. ③ DVOL at ~35% is a new cycle low and historically rare. SpaceX, ARMA, CLARITY Act — catalysts stacking, price not moving. No strategy this week. DVOL recovering above 45% is the re-entry signal. Until then: watch, don't trade. |