Bybit Options Weekly Review: April 8–14

Week of April 8–14, 2026

I. Weekly Market Recap

This past week was the most eventful of Q2 so far.

Within 72 hours, the world has lived through a ceasefire whiplash, the debut of Wall Street's first bank-issued Bitcoin ETF, a dramatic peace-talk collapse and now potential revival, and a U.S. naval blockade .

Still, the net effect of these macro events have resulted in risk-on mode, driving BTC from $67k to nearly $75k.

Price Action:

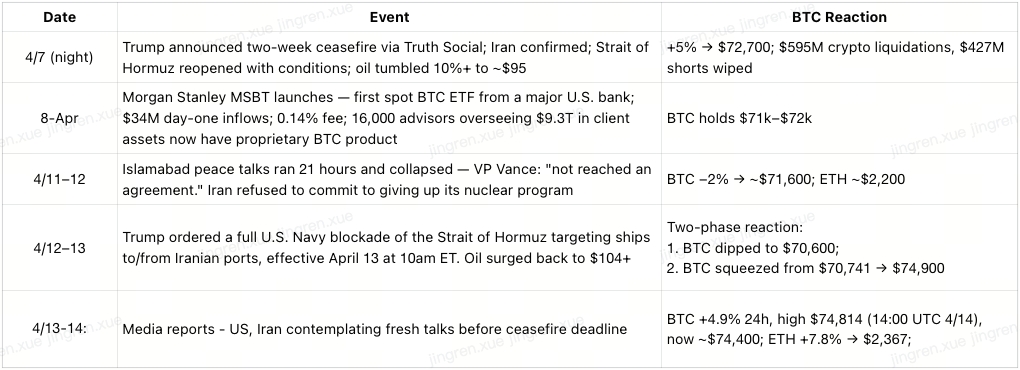

BTC: Week opened ~$67,500 → surged to $72,700 on the April 7 ceasefire announcement → held ~$73,000 into Saturday → dropped ~2% to ~$71,600 after Islamabad talks collapsed → squeezed back toward $74,900 on April 13 as Trump ordered the Strait blockade

ETH: Moved above $2,200 on April 8 — its highest level since March 18, holding ~$2,191–$2,238 into week-end

Net weekly change: BTC +10%+; ETH +7%+ — best week since Q1 2025

Fear & Greed: recovered from 8 → ~30 (still Fear, but sharp sentiment reversal)

Event Timeline:

II. Options Market Key Data

Weekly Expiry (4/11) — Ceasefire Volatility Reset:

Post-Ceasefire Options Dynamics:

Shorts worth $431 million were liquidated in 24 hours — the largest since March 4. The ceasefire pushed the market violently, but the rally is cautious — without fresh demand, gains can quickly reverse.

Bitfinex margin long positions remain above 80,000 BTC, indicating leveraged longs have not been reduced — crowded long positioning heading into the ceasefire expiry window (~April 22) is a risk.

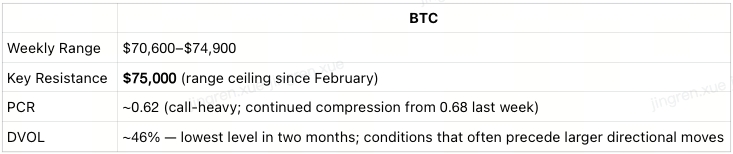

DVOL compression to ~46% is notable — the low-IV environment historically precedes breakouts. Flat-to-negative funding rates confirm the rally is driven by spot demand, not leveraged speculation.

ETF Flows — Structural Shift:

Crypto ETFs posted $1.14 billion in weekly inflows — the best since January — led by BlackRock's IBIT ($612M).

More notably, Ethereum ETFs reversed months of outflows as ETH outperformed BTC, signaling a shift toward diversified crypto allocation.

Meanwhile, Morgan Stanley's low-cost Bitcoin ETF (0.14%) opens the door to 16,000 financial advisors, marking a structural distribution milestone.

III. Macro Background

U.S.–Iran War (Week 7, Days 43–49):

The ceasefire is provisional — Iran's acceptance was conditional, and the Strait reopening came with hedges around "technical limitations" and "coordination with Iranian armed forces."

The ceasefire expires around April 22. IEA chief Fatih Birol warned April will be worse than March as pre-war shipments that cushioned the first month have all been delivered. Emergency reserves are forecast to run dry in mid-April.

Oil is still $30 higher than before the conflict started February 28. For oil to fall further, Hormuz tanker traffic and insurance rates need to normalize to pre-war levels.

Another round of U.S.-Iran talks is reportedly being planned for as early as April 15. Pakistan urged both sides to keep the truce. But Iran's parliament speaker returned from Islamabad saying they "will not bow to any threats."

Federal Reserve & Macro:

FOMC Minutes (4/8) confirmed hawkish tilt — no rate cuts signaled for near term.

Markets tepidly pricing Fed rate cut back in for 2026 - 42% chance of 25-bps cut by Dec 2026 - helps crypto stay bid.

FOMC meeting April 28–29 is the next major macro event; CLARITY Act markup window opens this week in the Senate.

March CPI (Released April 10):

Headline CPI jumped 0.9% month-on-month in March, with the year-on-year rate surging to 3.3% — a near two-year high, up sharply from 2.4% in February. Energy costs drove more than three-quarters of the monthly gain, led by a 21.2% m/m surge in gasoline prices.

Core CPI (ex-food & energy) rose 0.2% m/m — a tick below consensus — and 2.6% year-on-year, up from 2.5% in February. Services inflation moderated to 0.2% m/m.

Nothing unruly (yet) in core CPI in the first month of Middle East conflict. However, surge in energy costs is likely to pressure other goods and services higher in the months ahead.

Fed futures were largely unchanged following the release, currently pricing in just 8 basis points of rate cuts by year-end.

IV. Outlook for Next Week (April 15–21)

$75,000 is the line. Ceasefire expiry (~April 22) is the clock.

⚠️ BTC's next move depends almost entirely on what happens at the Strait of Hormuz. Until the strait reopens to full operation, the war will keep dictating Bitcoin's price action. A clean breakout above $75k on volume opens the path to $80k; a ceasefire collapse retests $65k–$68k.

Three Scenarios:

V. Trading Strategy Recommendations

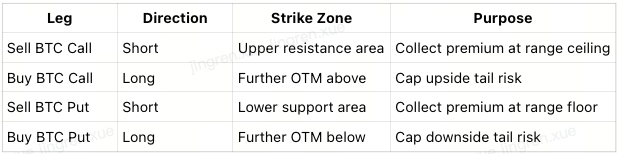

✅ Strategy — Iron Condor(4/24 expiry)

Rationale: DVOL has compressed to its lowest level in two months (~46%), making option premiums relatively cheap on the buy side and reducing the cost of protective wings. Meanwhile, the next two weeks will carry a cluster of binary catalysts — ceasefire expiry (~4/22), FOMC (4/28–29), and CLARITY Act markup — each capable of breaking the range, but none guaranteed to do so. The base case remains range-bound price action between support and the two-month consolidation ceiling, making a defined-risk premium collection structure the optimal fit.

Structure

P&L Profile (⚠️ The P&L diagram below is provided for illustrative purposes only. Actual breakeven levels, maximum profit, and maximum loss will depend on live option premiums, bid-ask spreads, and IV at the time of trade entry. This is not financial advice.)

Max profit: Net premium collected — achieved if BTC expires anywhere within the inner strikes

Max loss: Wing width minus net premium — fully capped on both sides, no unlimited downside exposure

Breakeven range: Approximately $67k on the downside and $76k on the upside, per the reference diagram

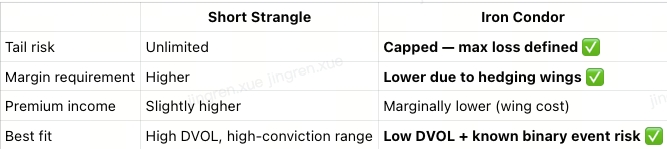

Why Iron Condor over Short Strangle here

Key risk events to monitor

~4/22 Ceasefire expiry — extension = Call side safe; breakdown = Put side at risk

This week CLARITY Act Senate markup — positive outcome = potential upside catalyst

Position sizing note: With DVOL compressed, the cost of protective wings is relatively low — this is a favorable environment to run the full four-leg structure rather than a naked strangle. Recommend keeping total notional exposure conservative (~50% of peak sizing) ahead of the 4/22 ceasefire window.

Risk Warnings:

Ceasefire expires April 22 without extension = rapid reversal toward $65k–$68k; exit short Put, let long Put ride

Clean break above $75k on volume = short squeeze to $80k+; Call side faces assignment risk — set stop

Next round of U.S.-Iran talks — outcome binary; hold reduced sizing (~50% of peak) into the event

🏆 Weekly Summary:

Most eventful week of Q2: ceasefire → Morgan Stanley ETF launch → Islamabad talks collapse → U.S. Navy blockade — BTC whipsawed from $67k to $74.9k.

Every sentiment and positioning indicator was pointing bearish before the ceasefire — the violent reversal reflects just how extreme the short positioning had become.

The structural picture has improved: DVOL at 2-month lows, first major bank ETF live, BTC up 8.64% in Q2 — but ceasefire expiry (~April 22) keeps a hard ceiling on conviction.

The ceasefire remains a pause rather than a durable settlement — conditional on how Iran and US manage passage through Hormuz over the coming weeks.

Options playbook: DVOL compression favors selling vol now; Short Strangle + Put Diagonal both viable — but keep sizing at 50% and treat April 22 as the real test.