Bearish positioning builds across crypto derivatives

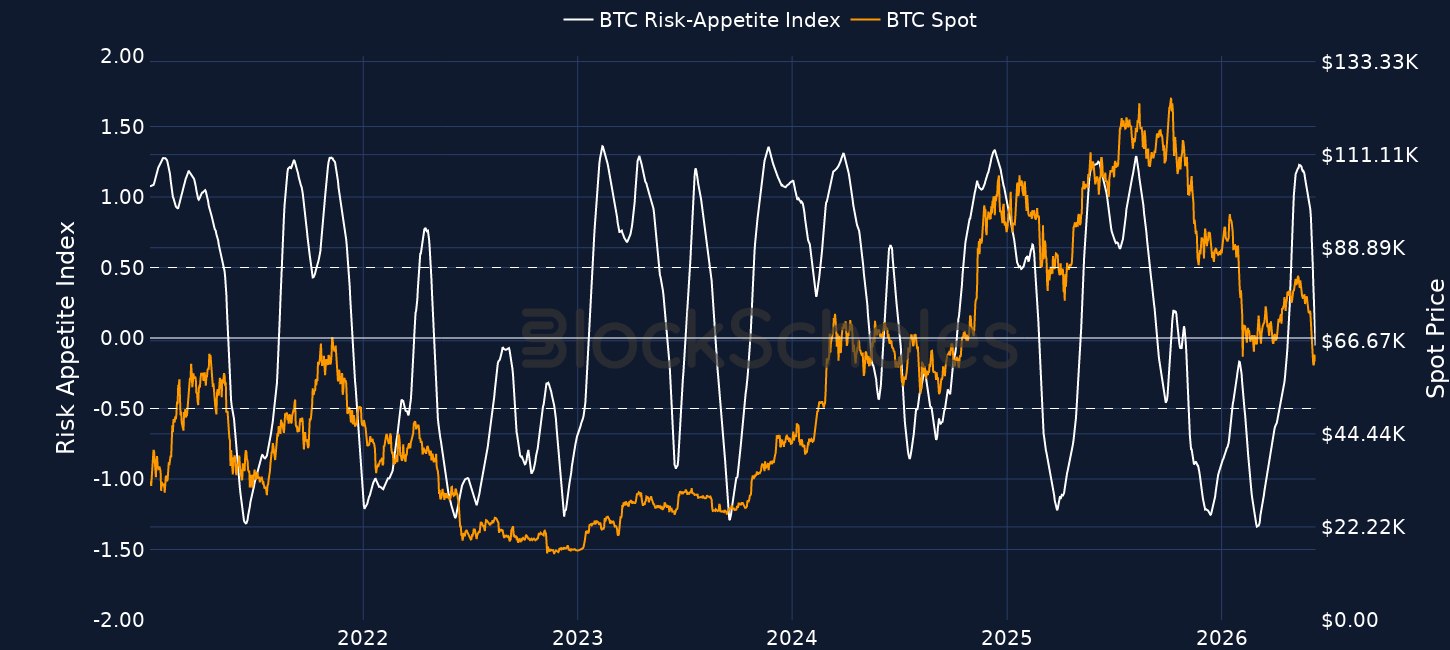

An almost 20% drop in BTC’s spot price last week has been reflected by a significant leg lower in our Block Scholes Risk Appetite Index.

READ MORE (published June 5th): Cryptos this week - BTC, ETH crash; TRON hits downside target; HYPE hits new record high!

That selloff was driven by a confluence of factors:

A June 1, 2026 filing from the largest BTC digital asset treasury company, Michael Saylor’s Strategy Inc., announced that the firm had sold 32 of its 845,256 BTC hoard. While a seemingly insignificant amount relative to the firm’s total holdings, markets took the disclosure as having undermined confidence in the digital asset treasury model Strategy has pioneered. However, a subsequent filing a week later, on June 8th, revealed that Strategy resumed buying during the week of June 1-7th, snapping up 1,550 BTC.

The longest spot Bitcoin ETF outflow streak since launch, which, after a brief pause, has continued once again.

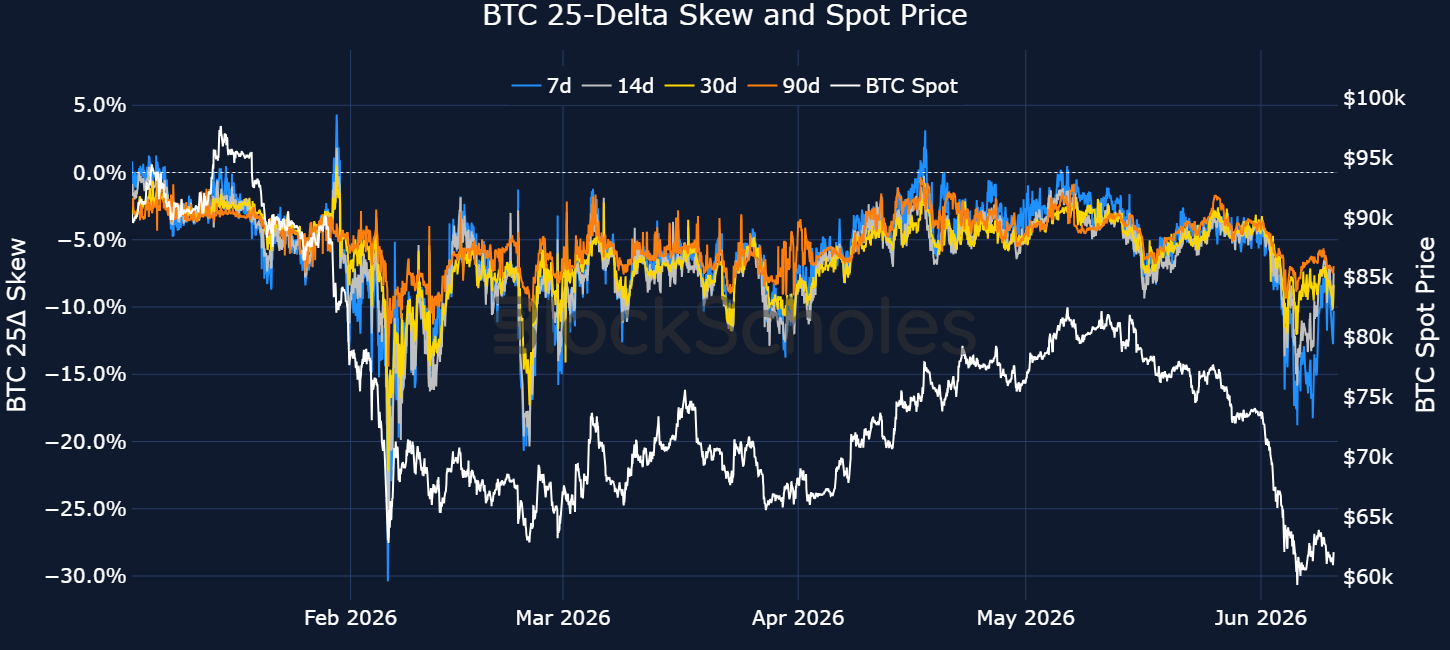

A continued rollercoaster of headlines around the Middle East conflict and dimming prospects of a Tehran-Washington peace deal.As such, last Friday (June 5, 2026), BTC fell below $60K for the first time since October 2024.READ MORE (published June 2): Bitcoin sinks below $70k for first time in 2 months! Here's why.The impact of a sub-$60K BTC price has, most meaningfully, been felt in derivatives markets. 7-day BTC put-call skew traded at -19%, as traders showed a strong willingness to pay a significant premium for downside puts over upside calls.

That revealed a market positioning for, and protecting against, further drops in spot price.

The last time short-dated skew traded that negatively was in late February 2026 when spot price fell below $63K after President Trump’s announcement to raise global tariffs to 15%.

DECODE: 25-delta skew: the implied-volatility gap between equally out-of-the-money puts and calls; a more negative reading means traders are paying up for downside protection

While skew has since abated from those deeply negative levels, traders still show an outsized demand for protection as short-dated skew still trades at -9%.

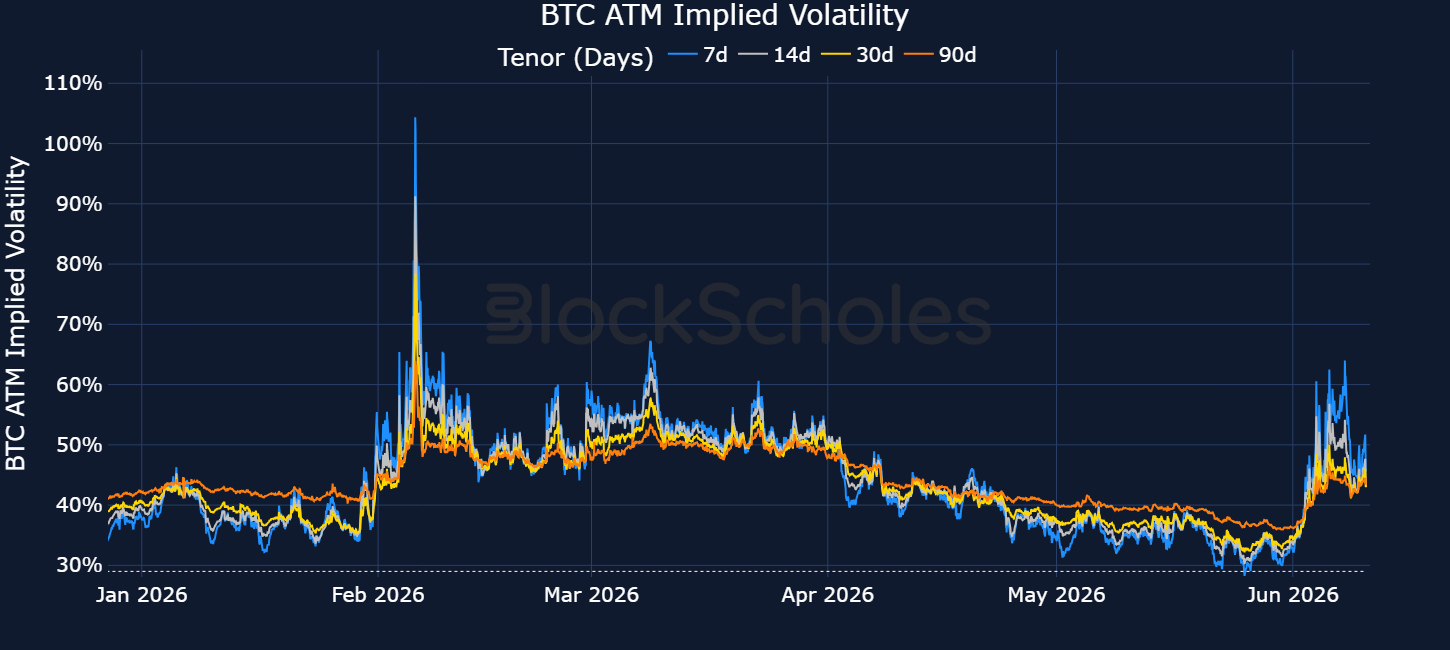

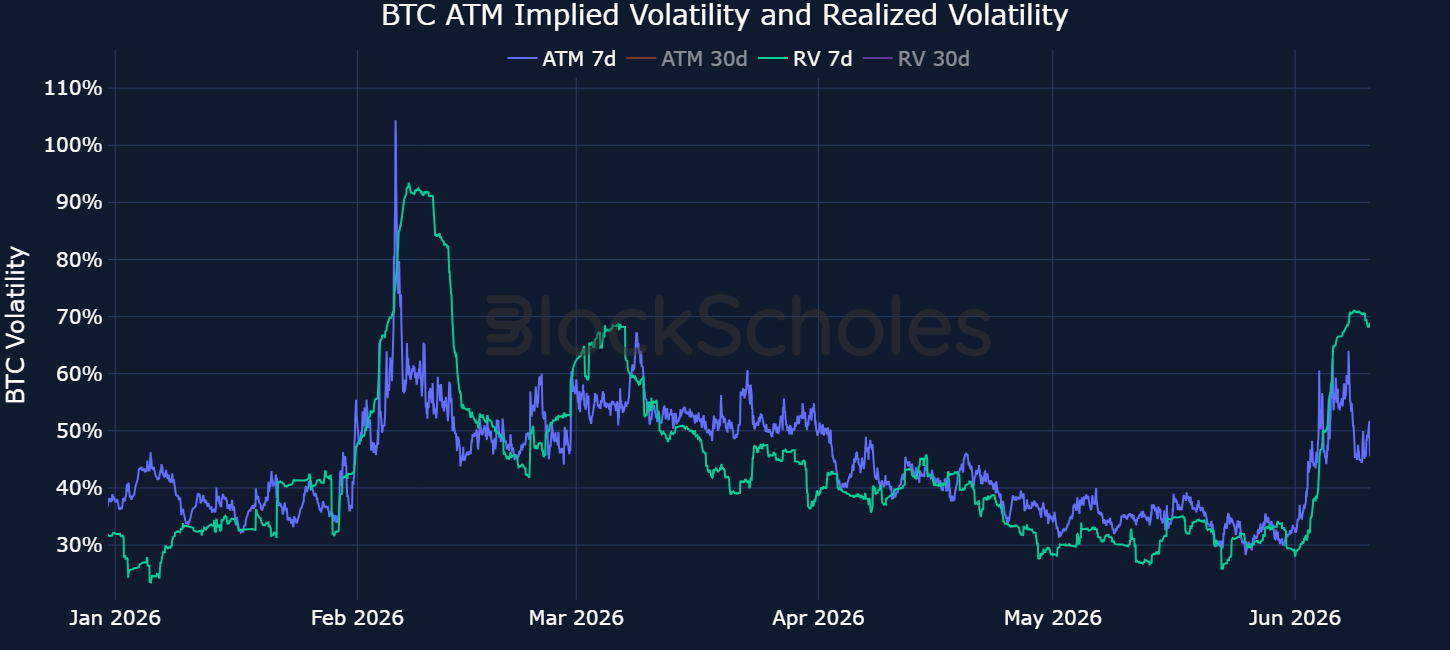

At-the-money implied volatility, the market's forward-looking estimate of how much volatility BTC will trade with over a future period of time, jumped to as high as 64% as spot price fell below the key $60K support level.

That was close to a 2x jump from June 1, when 7-day ATM IV traded at just 34%, close to a year-to-date low.

Since then, implied has fallen 20 percentage points down to 45%. The term structure of at-the-money implied volatility is now only modestly inverted.

In other words, short-dated options still trade at a premium over longer-tenor contracts, though that premium has compressed over the past few days.

Interestingly, while the premium traders demand for at-the-money options has dropped again, 7-day realized volatility, a measure of how much volatility BTC has actually traded with over the past 7 days, has remained significantly high.

From June 1, realized volatility more than doubled from 29% to 71%.

That now means options markets now expect BTC to trade with a much lower volatility over the next 7 days than what has recently been delivered.

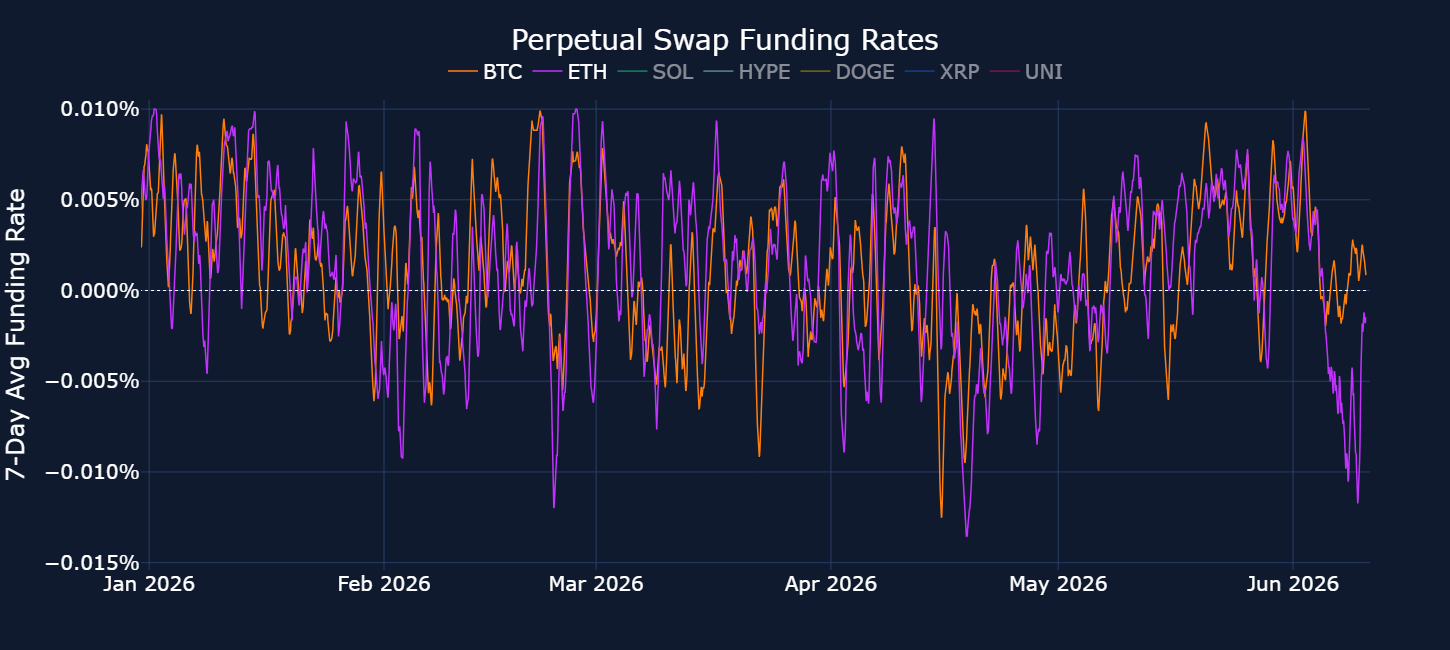

The same bearish positioning is also apparent in perpetual futures markets.

The 7-day rolling funding rate for ETH — a rolling average of the periodic payments exchanged between longs and shorts to keep the perpetual contract anchored to spot — fell below -0.01% for only the 3rd time this year.

The last time it fell to this level was on April 19, 2026, when President Trump threatened to significantly intensify the conflict with Iran should it not agree to a ceasefire.

DECODE: Negative funding rates indicate short traders are willing to pay longs to keep their position open. This is a sign that demand to be short outweighs demand to be long, and that traders are willing to pay a premium to express bearish exposure.

READ MORE (published June 9): Bybit Options Weekly Review (Jun 2–Jun 8)

DISCLAIMER:This article is provided for general information and reflects the author’s views only. It does not constitute investment advice, nor an offer or solicitation to buy or sell any financial instruments or digital assets. Your ability to access or use any products or services mentioned may be subject to the laws and regulatory requirements of your jurisdiction.