Understanding IPO pricing: from bookbuilding to final price

You find a high-profile IPO you want to join, like SpaceX, and instead of a single price you see a range. Maybe $25 to $28 per share. That range is not the final price, and it can change before you receive your allocation. This article explains why, and walks you through each stage from indicative price to final allocation.

Key Takeaways:

The indicative price range is a preliminary estimate. The final offering price is set only after bookbuilding reveals actual investor demand.

In traditional IPOs, underwriters arrive at the indicative range by looking at comparable companies, market conditions and early investor feedback.

If demand exceeds supply, allocation is distributed pro rata (proportionally based on subscription size), so you may receive less than you requested.

Where does the indicative price range come from?

Before a subscription window opens, an indicative price range is published. This is the underwriter's preliminary estimate of what investors may be willing to pay. It is not the final price.

In traditional IPOs, underwriters (the investment banks managing the offering) typically consider several inputs when setting this range. One of the most important is comparable company valuations. Underwriters look at similar public companies in the same sector and assess how they are valued relative to revenue, growth and market capitalization. A company with strong revenue growth entering a hot sector will generally command a higher pricing valuation than one in a slower-growth space.

Market conditions also matter. If broader equity markets are strong and investors have appetite for new listings, the range may be set higher. If markets are volatile or recent IPOs have underperformed, underwriters tend to be more conservative.

Early feedback from institutional investors, collected during pre-launch roadshows, can also shift the range. If large funds signal strong interest, the underwriter may push the range up. If feedback is lukewarm, the range comes down.

The key thing to understand: the indicative range is a planning reference, not a commitment. It tells you roughly where the price might land, but the final number depends entirely on what happens during bookbuilding.

What is bookbuilding?

Once the subscription window opens, demand is collected from investors. This phase is called bookbuilding, and it is the mechanism that turns the indicative estimate into a confirmed price.

In traditional IPOs, institutional investors (pension funds, asset managers, hedge funds) submit orders at various price levels. The underwriter tracks total demand, where it clusters within the price range and the quality of investors placing orders. This data forms the "order book" and gives a clear picture of what price the market will actually support.

On Bybit IPO Express, users participate by submitting a Conditional Offer to Buy (COB). A COB is a non-binding indication of interest showing you intend to participate based on the indicative pricing available during the subscription window. It is not a confirmed purchase, and the equivalent amount of USDC is frozen in your account until allocation is finalized.

Bybit aggregates all COBs during the window (total participants, total notional amounts) and passes this demand data to the xStocks issuer, who forwards an aggregated report to the underwriter.

Strong demand during bookbuilding may push the final price toward the top of the indicative range or, depending on the offering terms, above it. Weak demand may bring it lower. This is why the indicative price and the final price are rarely the same number.

How the final price is set

After bookbuilding closes, the issuer and underwriting syndicate review the full order book and set the final offering price. All allocations settle at this price, not the indicative range you saw when you subscribed.Why it may differ from the indicative range:

Demand was stronger or weaker than the preliminary estimate anticipated

Market conditions shifted during the subscription window

The order book revealed a different price concentration than expectedUsers searching for a SpaceX IPO price should understand that any figure shown before final confirmation is indicative, not settled. The final offering price is confirmed only after the full demand aggregation and underwriter review process is complete.

How your allocation is calculated

If the IPO is oversubscribed (more demand than available supply), allocation is distributed pro rata: proportionally based on your subscription size relative to total demand.

Here is a simple example. Suppose investors collectively request $100 million worth of tokens and only $50 million is available. Each investor receives approximately 50% of their requested amount. If you subscribed for 1,000 USDC, you would receive around 500 USDC worth of the offering, and the remaining 500 USDC would be unfrozen and returned to your account.

If total subscriptions fall below available supply, all subscribers receive their full requested amount.Submitting a subscription does not guarantee a full allocation. It guarantees participation in the process, not a fixed outcome.

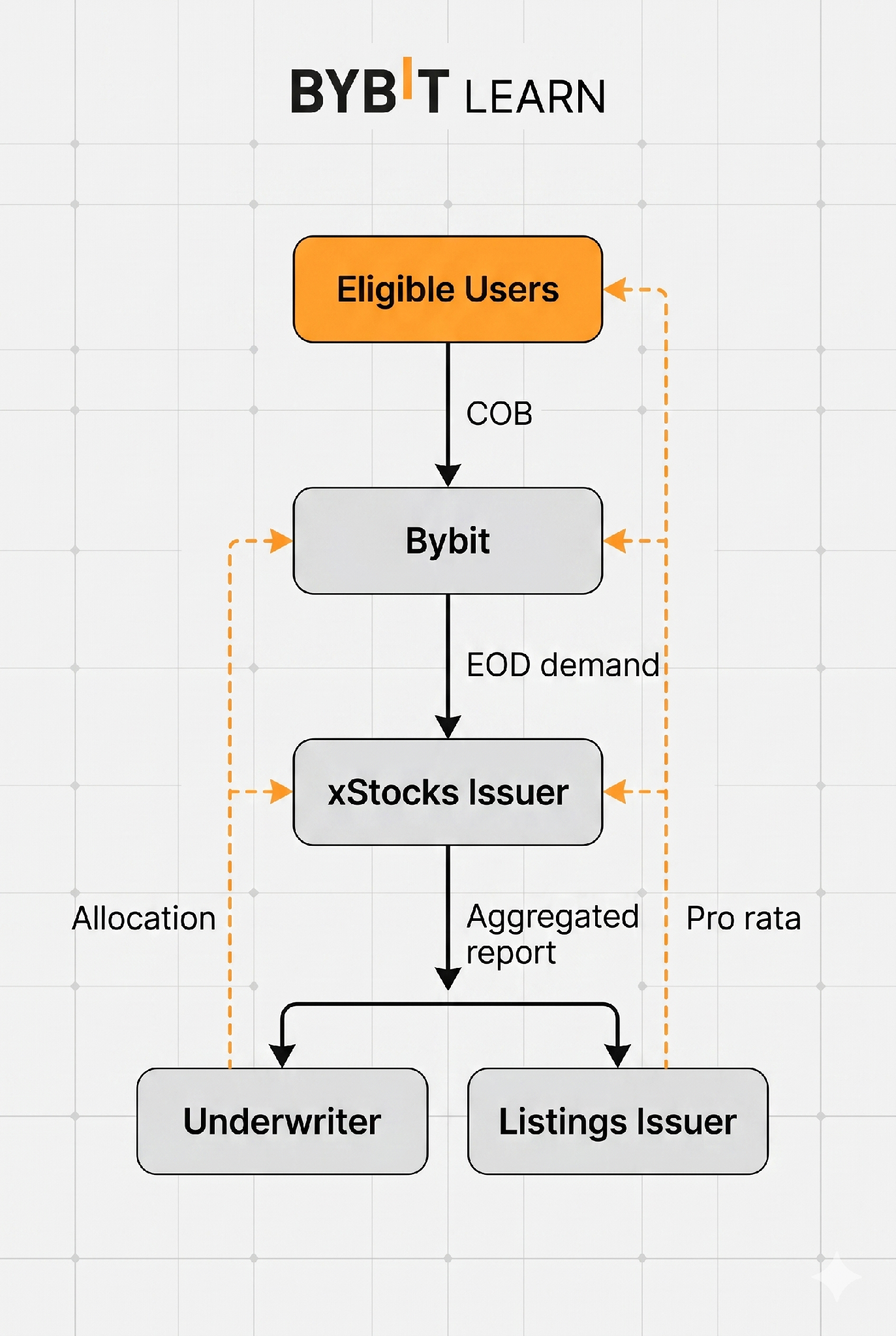

How this works on Bybit IPO Express

On Bybit, the pricing and allocation process runs through multiple parties. Using SpaceX IPO Express as an example:

1. You submit a COB during the subscription window.

2. Bybit compiles total demand (number of users, notional amounts) at end of day and passes it to the xStocks issuer.

3. The xStocks issuer prepares an aggregated report and forwards it to the underwriter.

4. The underwriter and listings issuer determine the final offering price and confirm the allocation algorithm.

5. Allocation flows back through the xStocks issuer to Bybit, and you receive your pro rata allocation as xStock tokens.

This multi-party process is why final pricing and allocation are not instant. Demand must be aggregated, reported upward and confirmed before results are distributed back to users.

The bottom line

IPO pricing is a process, not a fixed number. The indicative range gives you a planning reference, bookbuilding reveals demand and the final offering price is confirmed after the issuer and underwriter review the order book. Allocation is proportional, not guaranteed, so an oversubscribed offering may result in a partial fill.

On Bybit IPO Express, this process involves multiple parties, including Bybit, the xStocks issuer, the underwriter and the listings issuer. Understanding that flow helps you set realistic expectations for both the final price and the number of tokens you may receive.

#LearnWithBybit